G

Gareth

Member

This bit of the question is discussing how delta for a put changes as you get closer to expiry:

"Term decreases: The magnitude of the Put option delta varies as time progresses and the time to expiration of the option reduces, whilst always remaining negative. When the option is at or out of the money, the magnitude of the delta will tend to increase as the option expires. If the option is deeply in the money, then the magnitude of the delta can decrease as time progresses, although close to maturity it may still increase. (A plot of magnitude of delta against time may have a turning point.)"

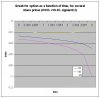

Let's look at the graph of delta for a put:

(see wilmott page 368 to verify this graph is correct)

Out of the money means S > K (so that max(K-S,0)=0). This means we are on the right side of the graph. Notice that delta gets smaller in magnitude (i.e. closer to 0) as we get closer to expiry... (expiry here is t=1, so t=0.9 is close).

Ok, so to be in the money, we need S < K. We are on the left. Here we can see that delta gets closer to -1 as time progresses. Again this is the opposate to what the examiner says.

So is the answer wrong, or do i have a misunderstanding here?

"Term decreases: The magnitude of the Put option delta varies as time progresses and the time to expiration of the option reduces, whilst always remaining negative. When the option is at or out of the money, the magnitude of the delta will tend to increase as the option expires. If the option is deeply in the money, then the magnitude of the delta can decrease as time progresses, although close to maturity it may still increase. (A plot of magnitude of delta against time may have a turning point.)"

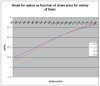

Let's look at the graph of delta for a put:

(see wilmott page 368 to verify this graph is correct)

When the option is at or out of the money, the magnitude of the delta will tend to increase as the option expires.

Out of the money means S > K (so that max(K-S,0)=0). This means we are on the right side of the graph. Notice that delta gets smaller in magnitude (i.e. closer to 0) as we get closer to expiry... (expiry here is t=1, so t=0.9 is close).

If the option is deeply in the money, then the magnitude of the delta can decrease as time progresses

Ok, so to be in the money, we need S < K. We are on the left. Here we can see that delta gets closer to -1 as time progresses. Again this is the opposate to what the examiner says.

So is the answer wrong, or do i have a misunderstanding here?

Attachments

Last edited by a moderator: