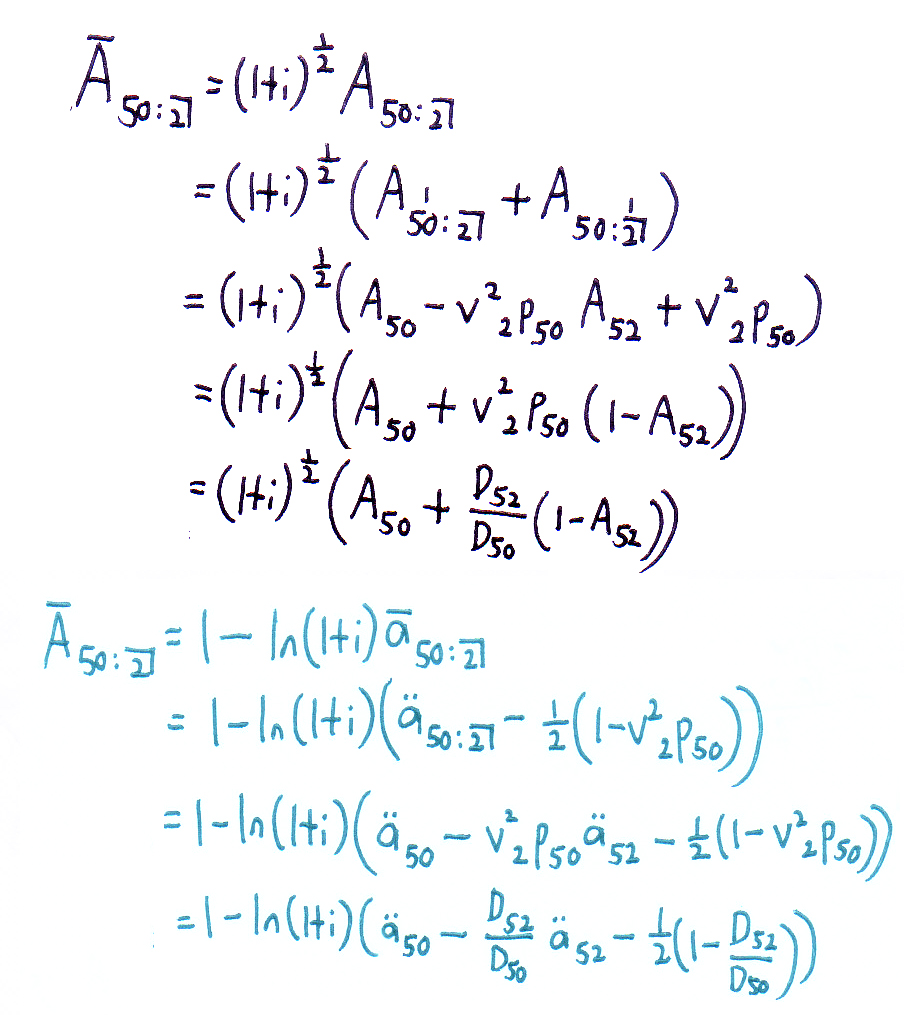

@Calm - your first approach (in black) doesn't quite work. This is because the survival benefit under this endowment assurance will always be paid at time 2. Applying the \( (1+i)^{\frac{1}{2}} \) to the whole \( \require{enclose} A_{50:{\enclose{actuarial}{2}}} \) means that you're bringing both the death

and survival benefits forward by half a year.

The correct approximation for an endowment assurance is \( (1+i)^{\frac{1}{2}} \require{enclose} A^1_{50:{\enclose{actuarial}{2}}} + \frac{D_{52}}{D_{50}} \) , i.e. you need to split the death and survival benefits up because the timing of survival benefits is always the same.